Analyse Economique

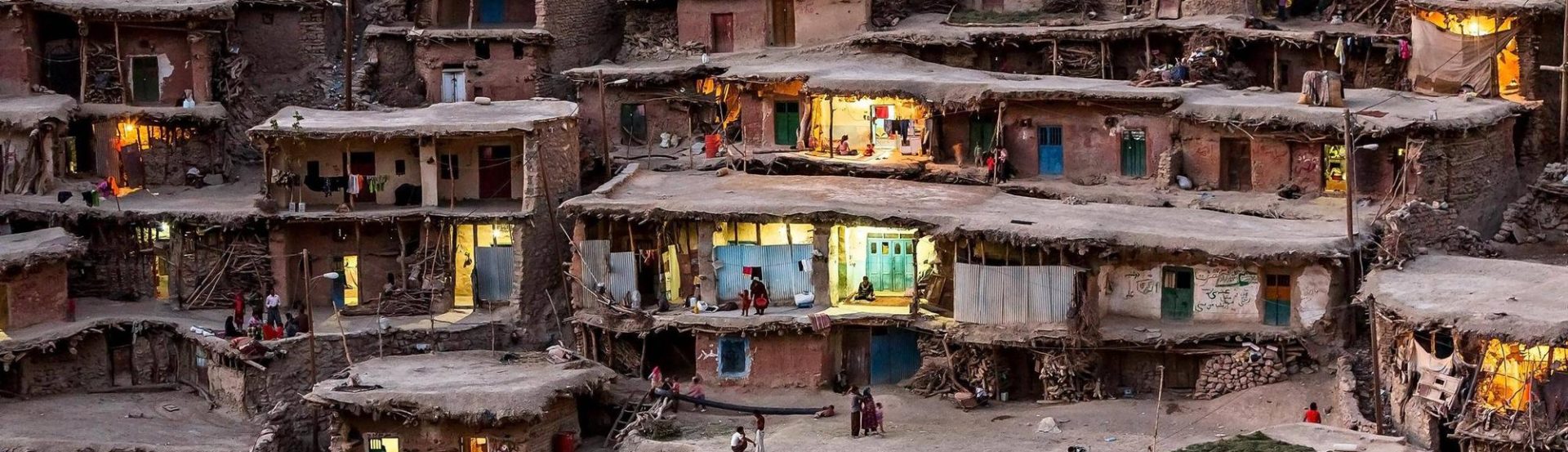

The current demographic boom in Africa has caused a rapid and dysfunctional urbanisation. Finding decent housing has become a serious problem. The continent has the fastest-growing urbanisation in the world. According to UN-Habitat, the urban population growth rate has reached 3 % per year. As a matter of fact, the urban population represented 40 % in 2009 and will reach 60 % in 2050 if the situation progresses at this constant rate. This uncontrolled urban growth has favoured the development and extension of precarious, unsanitary and unsafe slums. The population living in slums in Sub-saharan Africa has doubled between 1990 and 2012, from 102 million to 213 million (UNCHS data). Simon Walley[1] expects that the demand for housing will increase from 4 million in 2012 to 5 million in 2020. The public authorities have carried out many actions to make housing more accessible to disadvantaged people. Nevertheless, the problem persists and slums are expanding increasingly. Thus, only higher classes of the society can afford to live in decent houses. This situation deepens the gap between the rich and poor and requires a number of actions to guarantee housing for all. In this article, we shall look closely at the obstacles hindering the emergence of a real estate-market favouring poor people in Africa.

In an effort to counter the expansion of slums, public authorities, in South Africa and Ivory Coast, have chosen to build free or low rent social housing. However, these policies did not favour the targetted poorer population and civil servants took advantage of these measures. Due to a growing demand and lack of public financial ressources, these types of programs were not sustainable. So, the government decided to turn to the private sector for the construction of housing at a low cost. The State, in Angola for example, supported the private sector by giving a massive amount of subsidies. These programs were not very successful because they only took into account cost reduction and were not planned out and conceived for regional development. Most of the houses were built far from the main infrastructures such health centres, transportation and schools.

In theory, the demand for housing is almost unlimited. People who have a decent house wish for a bigger and more confortable one while those who do not have a decent house want one. However, this demand is not met in reality especially for financial reasons. According to the World Bank, in 2011, less than 5 % of the Sub-saharan African population took a loan to buy a house whereas in the USA or in Canada, this rate reaches 25 % to 35 %. These figures show us that the low-income households are excluded from the financial system because they represent a higher risk for credit institutions. The lack of financial culture can also explain why they do not have the sufficient ressources to be elligible for the acquisition of a house.

On the other hand, private real estate developers face many bureaucratic, regulatory and financial hurdles. Economic development is hindered by the slowness of administrative procedures in Africa, specially in the present case. Many social real estate development projects are blocked by regulatory constraints to access to property (which are rare and expensive in the urban areas). Furthermore, it is difficult for real estate developers to obtain long-term funds because credit institutions are quite reticent to finance social construction projects. In addition to these difficulties, the construction costs can be very high and qualified labor force and basic infrasctructures (such as roads, electricity, sanitation, etc) might not be available.

The failure of the attempts to solve the housing crisis in Africa reveals the importance of a better analysis of the needs of the population and a better consideration of the environment of the houses. We need a paradigm shift to implement sustainable housing policies on a larger scale. A policy that will involve all the operators in the sectors in different fields and take into consideration key-factors, such as real estate availability, types of leases authorised, funding of the sector and construction of infrastructures. Many experts will have to be consulted : demographs, land planning specialists, economists, insurrance providers, civil engineers, road specialists, etc.

Moreover, given that public ressources will not be sufficient to fund the housing needs, a collaboration with the private sector is necessary. Superficial subisidies to the private sector will not be efficient. The solution here is to implement incentive measures which will have a leverage effect. Public authorities should develop a positive environment for private investors and set specific rules and regulations to garantee the stability of the system.

The first step would be to secure and develop property. In fact, the property regulations are highly insufficient in Africa because they are made up of a combination of customary and state norms. Thus, the issuance of property titles are undoubtedly very difficult and property law lacks clarity. In some countries (such as South Africa, Uganda and Ghana), reforms shall be carried out to integrate customary norms in the national regulatory framework. Other regulatory measures including land parcelling following a cadastre model, simplification of registration procedures, and establishment of collective rights can be implemented. Once the legal framework is set up, the State should reorganise the land planning. Due to the lack of infrastructures, property developers often have to bear additional costs which affect the price per unit of the housing facilities. Morocco ideally dealt with this issue by creating a parapublic body specialised in accomodation and land planning.

The other major issue is the funding of the sector. On one hand, the private land developers need to invest large sums of money to start their projects. On the other hand, householders have to borrow on a long-term basis to fund the acquisition of the land. As far as mortgages are concerned, the African market is worth a trillion dollars (CSAE 2012)[2]. The State should encourage access to long-term financial ressources and implement risk-sharing instruments, in order to promote the developement of the market. Banks specialised in housing finance would be a good solution as this would enable traditional banks to have access to long-term ressources with higher risk guarantees. The traditional banks would then issue real estate securities on the market which would be guaranteed by mortgage loans and finance traditional banks. Thus they would then, in turn, refinance the households. Another solution would be to implement a public-private partnership by entrusting the management of the construction project to a private company. The State would secure the property market with the required authorisations, the donors would invest the first necessary funds and the property developers would implement their project on behalf of the company managing the project. To attract the remaining fundings, the private investors would be requested to fund the project as senior debt[3] with a guarantee from the promotors of the project, the State and the donors.

The State should also take interest in the informal solutions implememented by the citizens. For instance, many households rent their houses with no regulatory framework. Land owners can rent their unsanitary accomodation for a high price, or demand the payment of 2 years rent in advance (Nigeria), thus creating high distorsions on the rental market. However, the regulation of the rental sector will meet the needs of all social classes (especially the lower classes) and generate tax revenues for communities. Self-building is another example of informal initiative that started from the bottom. Households earning informal revenues buy plots and build their own houses, often of lower quality, thus favouring the emergence of informal settlements. The State should not stop these types of initiatives but set up a framework and regulate the sector with the collaboration of private investors.

It is very crucial for African states to rethink their housing policies in order to counter the current housing crisis in the continent. These policies should create a positive framework for private initiatives because pro-active public policies have shown their limits in other parts of the world. Public authorities should focus their efforts on securing operations, risk-sharing and implementing targetted incentives.

Translated by Bushra Kadir

[1] Mobiliser le secteur privé pour un meilleur accès au logement. Secteur Privé & Développement n°19 : relever le défis du logement avec le secteur privé. Proparco.

[2] CSAE. 2012. Research on Urban Mass Housing workshop. St Catherine’s College, Oxford, 26-27 mars 2012. Available on http://www.oxiged.ox.ac.uk/index.php/events/ urban-mass-housing

[3] A « senior debt » has specific guarantees and its repayment is a priority unlike other debts.

Laisser uncommentaire

Votre adresse e-mail ne sera pas publiée. Les champs obligatoires sont indiqués par *

Découvrez les articles du même thème

I have developed a sustainable, low income rental community model and have even installed infrastructure. However I am unable to find the social networks that I may move forward with my social enterprise. Please help.