Analyse Economique

The need for coordination of economic policies in a monetary union is widely accepted, in order to adress various issues (inflation, debt, GDP, etc.), necessary to ensure the union viability. In a monetary union, macroeconomic targets can be managed according to its characteristics, whether by a specific authority (monetary authority or fiscal authority), or by two authorities. In the latter case, it performs the policy mix to handle the target. In this article based on a study[1] on the coordination of economic policy in the WAEMU, we are particularly interested in the control of inflation. For that aim, we will start by the analysis the inflation history in the area. After that, we will study the inflation determinants to finish by deducing the right policies to control inflation.

The need for coordination of economic policies in a monetary union is widely accepted, in order to adress various issues (inflation, debt, GDP, etc.), necessary to ensure the union viability. In a monetary union, macroeconomic targets can be managed according to its characteristics, whether by a specific authority (monetary authority or fiscal authority), or by two authorities. In the latter case, it performs the policy mix to handle the target. In this article based on a study[1] on the coordination of economic policy in the WAEMU, we are particularly interested in the control of inflation. For that aim, we will start by the analysis the inflation history in the area. After that, we will study the inflation determinants to finish by deducing the right policies to control inflation.

1. Inflation in the WAEMU : an overview

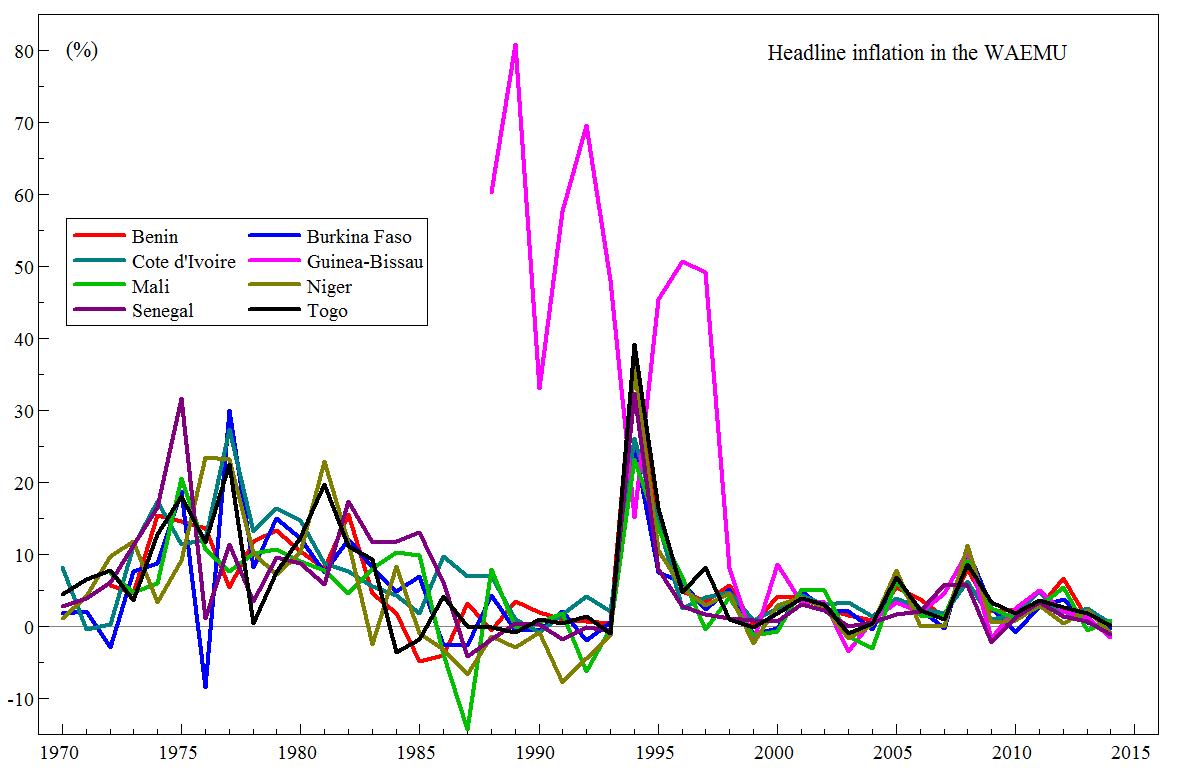

The chart below show the evolution of inflation in WAEMU between 1970 and 2015 except for Guinea-Bissau which joined the union in 1997.

Three main periods can be noticed in the evolution of inflation WAEMU:

- 1970-1994: This is the period before the birth of the WAEMU, characterized by a relative high volatility and significant amplitudes (from -15% to 30%);

- 1994: At the approach of the WAEMU birth (in 1994), there is a convergence of inflation levels. However, the devaluation occurred in the same year has resulted in historically high inflation levels. We can also notice that Guinea-Bissau had the highest desynchronized inflation until its admission to the union in 1997;

- 1994-2015: A clearer inflation convergence but sometimes there are inflation rate in double digits and negative inflation rate.

If the inflation was not stable over the time in the WAEMU, what are the factors behind the different variation during that period?

2. Inflation determinants in the WAEMU

The control of inflation within the WAEMU[2] is mainly entrusted to the Central Bank, BCEAO (Article 8 of the statutes) since countries independence (1962). At the birth of the economic union in 1994, governments have been associated in this management through the definition of convergence pact which imposed a maximum annual inflation rate of 3% in each member States (see Ouedraogo, November 2 2015, for details on the convergence pact criteria). The previous historical analysis clearly shows that inflation management remains difficult. Using an econometric approach to decompose inflation into short-term and long-term components, we inferred that the short-term component inherent to transitory items are most relevant to explain the inflation level. This explains the inflation volatility. This short-term component is affected by several shocks. On one hand, there are two common shocks in 1994 and 1987. The devaluation of the CFA franc in January 1994 led to higher prices (imported inflation) in all countries. The 1987 shock is attributable to the fall in the price of oil which has affected domestic prices. On the other hand, there are many idiosyncratic shocks (which affect a specific country). These idiosyncratic shocks are due to political instability (for example forced introduction in 1990 of multiparty politics in Cote d’Ivoire or military coup in 2003 which led to lower demand components in Guinea-Bissau), climate shocks in Benin (1985), in Burkina Faso (1976), in Mali (1992), in Niger (1991) or in Togo (1984). We can also notice that these idiosyncratic shocks have the most significant effects. In addition, inflation in the WAEMU is mainly determined by idiosyncratic shocks.

3. What is the appropriate policy to control inflation in the WAEMU?

The WAEMU inflation was initially managed by the BCEAO and in a second time by the policy mix since the birth of the economic union. Both management practices do not appear to have allowed inflation full control. Indeed, non-monetary origin of inflation is inferred in the literature. An article previously published (Ouedraogo, June 29, 2015) allowed to show the monetary transmission difficulties in the WAEMU and the marginal influence of monetary policy on economic activity. Inflation mostly explained by idiosyncratic shocks, so its control by a single and common tool is not efficient. That is why the period 1970-1994 was marked by significant levels of inflation and high volatility. If any shock affects and destabilizes a member State’s inflation, it is difficult for the BCEAO to change its monetary policy to only stabilize this inflation. This policy could destabilize inflation in other countries. It is the result of policy failures during the period 1970-1994. The policy mix does not seem very effective because it alternates periods of high inflation and disinflation since the BCEAO remains the main actor in inflation managing. It only remains the control of inflation by the governments. This management seems most efficient. Indeed, if inflation is mainly due to specific shocks, it should be handled with the domestic (national) tools that will respond quickly and efficiently. However, to ensure harmony within the union, the national management should be coordinated through the definition of an optimal threshold to be necessarily met by member States.

The proper control of inflation is necessary in a monetary union because inflation can influence other macroeconomic targets. High inflation may slow economic growth and deteriorate employment. Similarly a persistent negative inflation rates may lead to deflationary spiral that will lead to negative effects on growth and employment. This article shows that inflation should be managed by governments in the WAEMU because it is inherent to idiosyncratic items. Coordination of fiscal policies in order to ensure similar levels of inflation is also recommended. Furthermore, it should be noted that despite all these facts, the WAEMU area remains the most homogeneous area in Central and Western Africa.

Daniel E. T. Ouedraogo

Laisser uncommentaire

Votre adresse e-mail ne sera pas publiée. Les champs obligatoires sont indiqués par *